Summer 2022 Guide to Financial Planning

Photo by Kaizen Nguyễn on Unsplash

Let’s face it, for most people, the first half of 2022 has not been the best from a financial perspective. Inflation has been around 8% for some time, with little signs of slowing down so far, empty shelves are becoming the norm, and your savings may have taken a nosedive! What can you do?

The bad news is that you have no control over what inflation, interest rates, or market returns will be in the future. The good news is that jobs are plentiful and the pandemic is over. So, with summer in the air, let’s focus on what we can control to improve our financial situation despite the setbacks. Here are some ideas for money projects that you can take during some of your summer weekends, maybe with a smoothie or a margarita nearby. If you are new to planning, these ideas are a good way to get started and change the way you think about money. Enjoy!

Perform a Mid-Year Review of Your Finances

Summer is a good time to perform a midyear review of your finances, focusing on your cash flows. First, take a look at your year-to-date paystub. Start by comparing your gross income with your take-home pay, and learn about the different items of your pay stub, which determine how much is left for your checking account, as we do in this post.

As you review your deductions, make sure you are contributing your desired amount to your 401(k) and your HSA or FSA accounts. In previous posts, we recommended directing at least 10% of your gross income to your retirement account, and even more if you are a mid-career employee with above-average earnings. If you have room to increase your contributions, periods of low market values are a good time to invest more. While you are looking at your paystub, write down how much you have paid in federal income taxes so far this year. Then check that you are on track with your taxes, so you will have no surprises when you file your tax return next year.

Next, download all your transactions from your checking account and your credit cards. Add up all your inflows and your outflows. Your outflows will also include what you have spent using your credit card and haven’t yet paid. Once you add it all up, you may be in the red or in the black. If you are in the black, compare that amount to your take-home pay, and consider automating some of your net cash flow. Automating your investments in periods of market volatility and market lows is a great way to increase your potential long-term returns. If you are in the red from a monthly cash flow perspective, consider changing your budget, starting with our next project, your 50-20-30 targets.

Set Savings and Spending Targets with the 50-20-30 Rule

How much you contribute towards your goals (your saving rate) is a key determinant of financial success, more so than your investment returns. However, disciplined saving is hard to implement, particularly with many competing needs and wants, and a busy life. One tool to help you get started is the 50/20/30 rule.

The rule states that you should devote 50% of your after-tax income to your necessities, 20% to saving for your financial goals, and 30% to your wants. Your after-tax income can be computed from your paystub. Start with your gross income and subtract your tax withholdings (including Social Security and Medicare contributions).

Your necessities include rent or mortgage payments, utilities like electricity, water, gas, telephone bills, groceries, and basic clothing needs. Basic spending on transportation needs is also included. Your first saving goal should be to fund or replenish a safety net. Next is your retirement goal. Most people should start saving about 10% of their income for retirement. Higher earners should make this a starting point, and increase it over time to about 20%. Your wants include spending on entertainment, like eating out, movies, etc., and shopping for things you like, including electronics, hobbies, vacations, etc. It also includes spending more than strictly needed for a good or service.

Notice there is a reason we write it as the 50/20/30 rule, and not 50/30/20: saving for your goals has priority over your wants! Once you have set your targets based on your net income, the next step is to see how close or how far from the targets you are. If you are far off the targets, use the targets as goals to help you direct your income to the proper buckets. Learn more about this approach to setting savings and spending goals, and adapt them to your situation, in this post.

Make a One Page Financial Plan

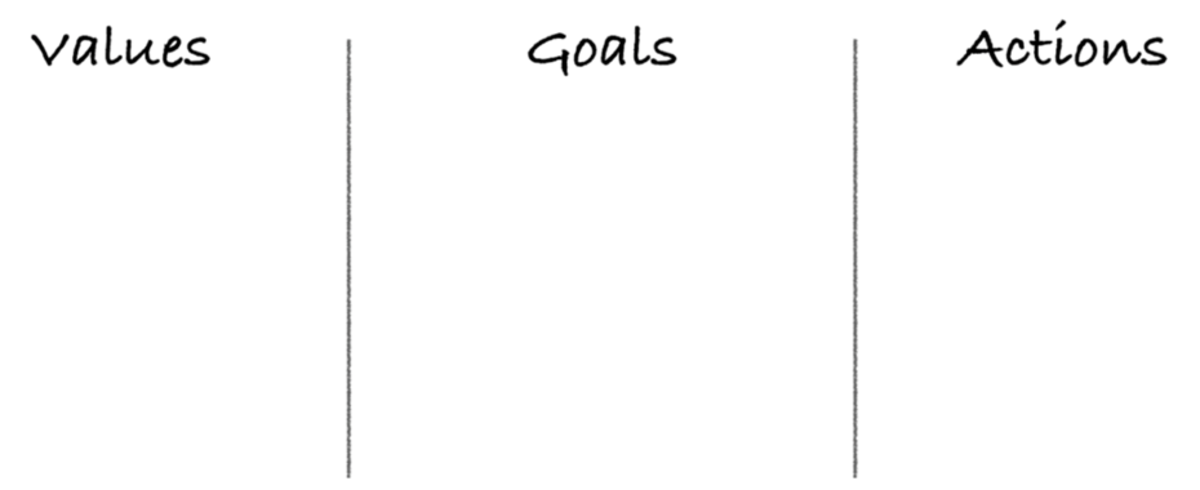

If you are not ready to engage a financial planner to help you plan, get started on your own with a one-page plan. A one-page plan can be accomplished by anyone in a few hours. It won’t be as detailed as a fully-fledged plan, but it carries many of the main benefits. It’s best to do this with a partner or a good friend. Take a piece of paper and divided it into three areas, like this:

Why this format? Values are the intangible things you care about, they are the WHY of your plan. Why is money important to you? Values provide the emotional payoff that’s required to take action, monitor progress, and ultimately achieve your goals. Goals are measurable objectives that require planning to achieve. They are the WHAT of your plan. Start from your list of values, and ask: what measurable result(s) will help me fulfill my values? This brings us to the actions list: “What can I do, starting today, that will get me closer to my goals?”

You may say, wait, there are no numbers or complex wealth strategies? That’s right. The point of this plan is to change your mindset, from just going through life to having a plan, a strategy to accomplish your most important goals. That is often the hardest step to accomplish. Once that is completed, you can start tackling individual goals. A complete step-by-step process to create your one-page plan can be found here, and if you need more help identifying goals, check out our process.https://0fe5c0e4c6cd8873f73bc09e301d87aa.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

Other Weekend DIY Projects

The three topics above help you take control of your financial life. After that, consider any of the following projects for you to tackle over the summer, with links to our posts on how to execute them:

- Build a Safety Net

- Get Financially Organized

- Create a Budget, part 1 and part 2

- Start Your Own Retirement Plan

- Control Your Spending

- Build Your Investment Guidelines

- Create a Goals-Based Investment Plan

- Optimize Your Portfolio

- Start a 529 Plan for College Savings

- Use Your Savings Efficiently

The Benefits of Financial Planning Projects

We cannot control how financial markets or the economy will perform in the future; we can only change our own behavior. Working on these projects helps you focus on what’s important to achieve your goals, and on elements you can control. By gaining a better understanding of your finances and being more focused on your goals, you can increase your confidence in your financial future. All of these projects have one thing in common: they provide you with measurable goals to work towards, help you improve your savings and spending habits, and provide a way to track your progress.

Even if the savings targets suggested here do not seem feasible, starting early and saving consistently what you can is the best way to get started. Going through these projects can help you move in additional directions, including creating a safety net, or an investment portfolio for long-term goals. Once you have attempted or completed these projects and learned the basics of financial planning, you may want to consider talking to a professional for help. A trusted financial planner can give you objective advice to help you navigate uncertain markets and make the most of your resources.

Massi De Santis is an Austin, TX fee-only financial planner and founder of DESMO Wealth Advisors, LLC. He is also a lecturer of finance and economics at Texas State University. DESMO Wealth Advisors, LLC provides objective financial planning and investment management to help clients organize, grow, and protect their resources throughout their lives. As a fee-only, fiduciary, and independent financial advisor, Massi De Santis is never paid a commission of any kind, and has a legal obligation to provide unbiased and trustworthy financial advice.

{kind=link}