Feeling Lucky or Smart?

Beating market averages appeals to our innate desires to be above average and to control outcomes in situations of uncertainty. But in the case of stock returns, the best course of action may be to embrace uncertainty, rather than trying to control it.

There is an experiment you can do in a large auditorium. You ask everyone to stand up and choose heads or tails. Then you flip a coin, and ask the ones with a wrong guess to sit down. If you start with 200 people, you expect 100 to be still standing after the first flip, 50 after the second flip, and so on. There is a good chance someone will be standing after 8-10 rounds. Is the person still standing a skilled coin guesser or just lucky?

Investment outcomes are the result of elements we control through our decisions, like asset allocation, and elements we don’t, including the state of the global economy, natural disasters, policy decisions, etc. With risky investments, we observe the outcome, a return, but often we don’t know whether the outcome is the result of our good decision making or just plain luck (elements outside of our control). Most of us aren’t naturally comfortable with the notion that we simply can’t control outcomes, and so we try to do something about it. This tendency can lead us to believe we may be good coin guessers. But often times the best we can do is to just embrace uncertainty, instead of fighting it. Here are some ways in which investors try to control portfolio returns. How well do you think they do it?

In or out of stocks?

One of the most talked about topics in the financial media is the market outlook for stocks. Is now a good time to be in our out of stocks? The idea is that by being smarter, more skilled, or having done more analysis than anyone else, some self professed expert can predict where the market is going. If you can do that, you can generate much higher returns than a simple buy and hold strategy without increasing risk. This is just the selling high and buying low wisdom everyone has heard before. It turns out the returns from being able to time the market are really high. Imagine getting all the upside of stock markets without any of the downside. You could beat Bernie Madoff without committing the fraud if you could time markets. That’s where the appeal of the strategy comes from.

Testing, testing, testing

Just like the coin flipping example, out of many managers trying to time markets, a few are bound to be successful, even by mere chance. Other managers may not have been successful yet, but will claim to have a good theory that can accurately call market turns. How can we find out if they offer true skill or just plain luck? Ask questions. It is not enough for a manager to just say have done it in the past, or that they can predict market turns by using more data than ever before, or with a new way of looking at the data. How did they determine that their strategy will work in the future? What tests have they run? Good predictive tests use at least two separate sets of data. Some data is used to design and refine the strategy (the training set), and some other data is used to test the strategy. Having a second set of data (some time called the out-of-sample data) is crucial in evaluating a strategy. Yet I bet you have never seen one out-of-sample test from the managers that claim to beat the market. Why is it a crucial test?

Stars, sunspots, and stock returns

It is actually quite easy to find some strategy that works well with past data. The question is whether the strategy is useful at predicting future outcomes. Robert Novy Marx, a professor of finance at Rochester, finds many examples of predictors that seem to be related to stock returns, including sunspots, the stars, and the weather. But surely you wouldn’t invest in a strategy based on sunspots. How is that possible? If we look hard enough, we can find variables that explain any observed pattern. Researchers call this ability data mining. Humans are good at it, and computers may be even better. But if the theory on which you base predictions is wrong, you are attributing outcomes to the wrong factors, and future predictions will be unreliable.

Show me the money

Next time someone claims they can time the market, ask them to show you their evidence, including out of sample tests. Rigorous testing, for example by researchers at Brown and Emory Universities, shows market timing strategies don’t survive out of sample testing. There are many variations of the market timing strategy. Some versions use macroeconomic and financial indicators, others use the statistical patterns of the market itself and, more recently, artificial intelligence and big data. Unfortunately, more data may not mean better prediction. Always ask for extensive out-of sample tests. Remember that to time the market you have to guess both when to get out and when to get back in (two hits in a row). Your hitting rate would have to be greater than 70% to have at least 50% chance of making timing work.

Which stocks should we pick?

There is no shortage of predictions about which stocks to buy and which ones to sell. Why would you hold an index of all stocks? Aren’t you better off with a few, carefully selected stocks? Research shows that across the universe of stocks, less than half of them beat the T-bills in any given year. And most of the wealth over the long term is created by a few stocks. So why not picking only the few good ones? If only it were that easy…If we knew ahead of time which ones are the good ones, yes, but do we? Just like coin flipping or market timing, by chance alone we would expect that certain managers, after the fact, emerge as great pickers. But were they lucky or smart? We need to be careful against data mining, so always ask for good out of sample evidence.

What’s the evidence?

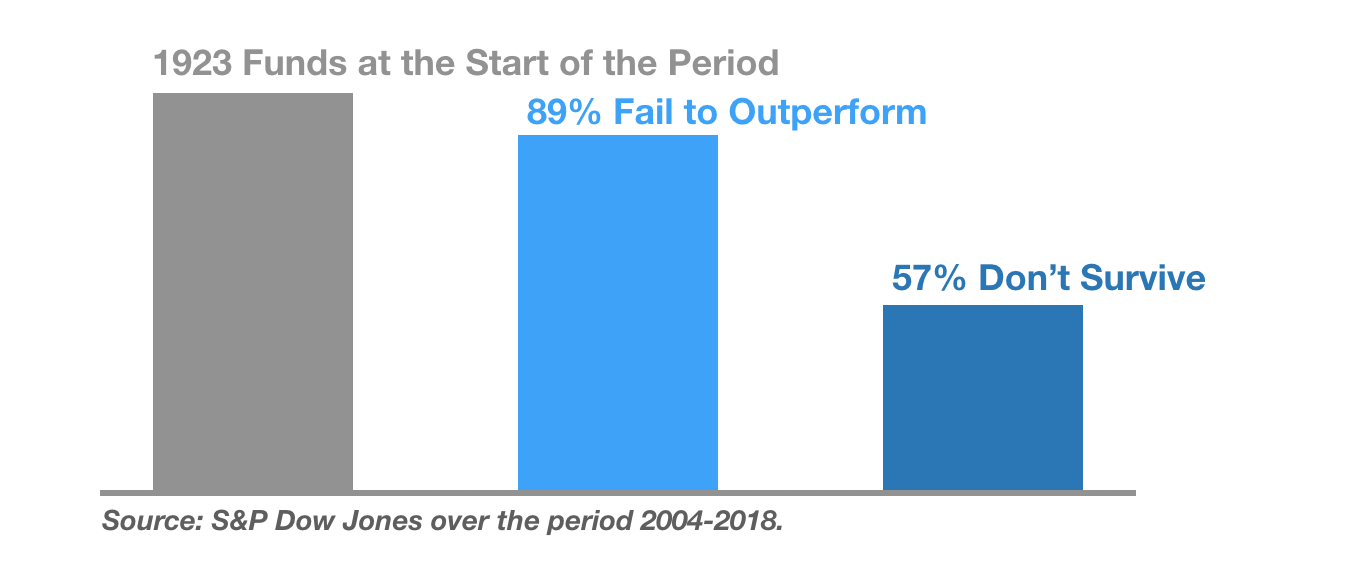

Academic studies have tested extensively the performance of managers that claim they can beat a market index after costs by carefully selecting stocks or industries. And the results? Here are some numbers from S&P Dow Jones for you to consider. Say you pick 100 active funds over the 15 year period ended in 2018. How many do you think were able to beat a market index? How many failed to do so? While 11% of the funds succeeded, 89% of the funds failed to beat a simple index.

Yes 89%. These are all active managers that presumably have some good theory for how they are going to select stocks or time markets. What’s worse is that of all the funds present at the beginning of the period, only 43% survived; 57% did not make it to the end of the period. When you pick an active fund for long term investments, keep in mind that more likely than not, that investment won’t be in your portfolio for the entire horizon.

We only like winners

OK you say, beating the market is hard to do, but 11% of the funds managed to do it, so why not pick one of those? But is past performance a reliable indicator of future performance? S&P Dow Jones data has the answer. If a fund is in the top 25% this year, does this make it more likely to be in the top 25% next year? By chance alone, 25% of funds will be in the top quartile next year. So, if past performance is an indication of future performance, you expect the likelihood of a top fund to be greater than that. Alas, the data shows that a top 25% fund in a year has only a 21% chance of repeating the following year. And there is more. How many of the funds studied by S&P Dow Jones stay in the top quartile over a 5 year horizon? Zero! Overwhelmingly, past performance is not a good metric of future performance. After all, if picking past winners was a reliable metric, who would ever invest in the losers to begin with? There is a reason why investment managers have to disclose that past performance is not indicative of future performance in any of their fund marketing materials.

What do I have to lose?

We aren’t saying no one can beat the market. But can you tell if the manager you are talking to is smart or just lucky? That’s the question that matters for investors. The evidence shows that there are so few cases of outperformance that it is impossible to tell a truly skilled manager from a lucky one with any certainty. Do you feel lucky enough to have found the smart one?

The risk you take by investing an active manager is twofold. First, there is a risk that in the pursuit of outperformance, you miss out on what the market has to offer, as the investors who got out of stocks this year are finding out. As of this writing the S&P 500 index is up 19% for the year. That’s going to be hard to make up for. Second, there is a high likelihood that your fund could die or merge into a different strategy in the next 10-15 years, which is a very common horizon in investing. Usually funds that do that are ones that don’t perform very well.

Can you behave?

There is more. The uncertainty about whether you have found a true outperformer adds to the overall uncertainty of the markets, and both can play a bad game on your emotions. I always ask my clients how they think they would behave if their investments dropped significantly in value (25% or more) or if they significantly lagged market returns. A lot of clients tell me they would sell or would consider selling. It helps me gauge their tolerance for risk. If that’s you, imagine how you would feel today if you got out of stocks at the end of last year. Would that make you doubt your ability to pick a market timer? Would you consider getting out of that strategy?

Unfortunately, there is no reliable way to beat the market on a consistent basis. I think deep down most investors know it, but as discussed last week, our emotional selves like to believe it is somehow possible. The emotions are driven by our innate desires to be better than average and to have control over uncertain outcomes. But in the case of stock returns, the best we can do is to embrace the uncertainty rather than control it. And the best way to embrace it is to rely on a strategy tailored to your risk preferences. Start by answering these questions to set investment guidelines and your strategic allocation. Then stay tuned for more!

Until next time!

Massi De Santis is an Austin, TX fee-only financial planner. DESMO Wealth Advisors, LLC provides objective financial planning and investment management to help clients organize, grow and protect their resources throughout their lives. As a fee-only, fiduciary, and independent financial advisor, Massi De Santis is never paid a commission of any kind, and has a legal obligation to provide unbiased and trustworthy financial advice.

{kind=link}