Image by Mediamodifier from Pixabay

A common investment thesis is that stocks are part of “real assets” and should protect long term investors from inflation. Corporate profits should increase by the amount of inflation, and since stocks represent the claim to future company profits, the value of stocks should also increase with inflation. As a result, real stock returns (returns adjusted for inflation), would be unaffected by inflation. This theory relies on the assumption that money has no real impact on the economy. But does the theory hold in practice?

Our research shows that stocks do outperform inflation on average and over time, both in periods of higher inflation and in periods of lower inflation. However, average real stock returns are lower in periods of higher inflation. So stocks are not a “hedge” for long term investors. Investors and financial planners should take the lower returns into account when making financial planning decisions.

What is an Inflation Hedge?

In absence of inflation, investors can expect their returns to fluctuate over time due to changes in economic conditions that are reflected in stock prices and stock returns. Inflation adds an additional risk for investors, by making it harder to anticipate the purchasing power of their future wealth. Inflation adds uncertainty to what investors really care about, which is real wealth.

In principle, real stock returns could have a positive, negative, or zero correlation with inflation. A positive correlation would mean that real stock returns tend to be higher than average when inflation is higher than average, while the opposite would be true with a negative correlation. With a zero correlation, we could expect stock returns to be the same in periods of higher and lower inflation. If real stock returns have a zero or positive correlation with inflation, stocks can help reduce inflation risk in a portfolio and would be considered a hedge for long term investors.

Inflation and Real Stock Returns

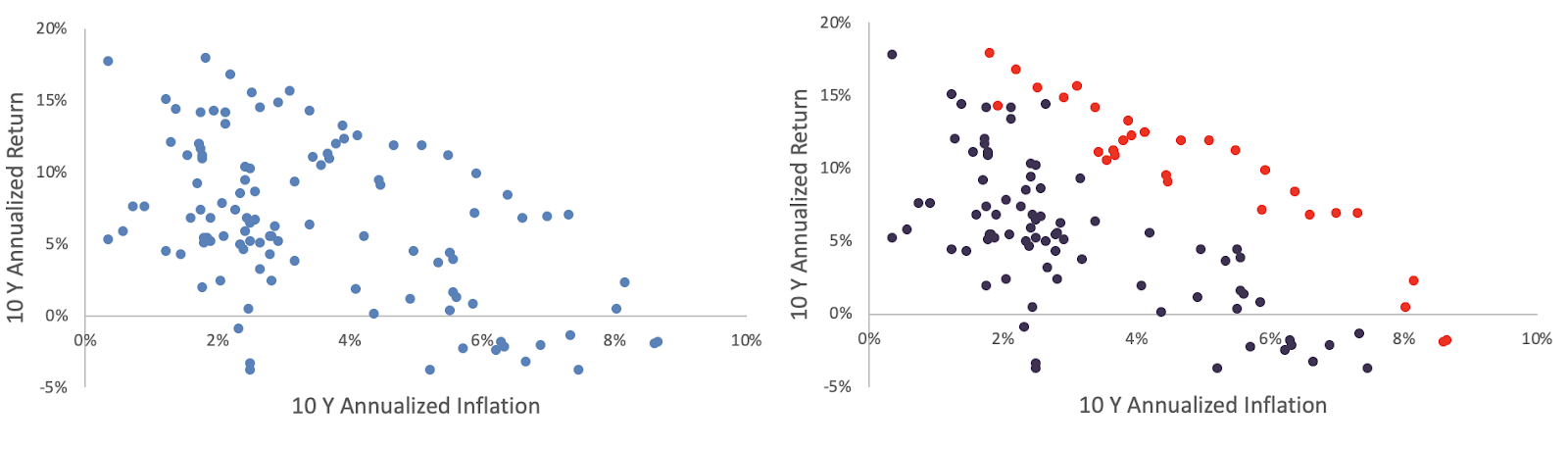

In the plot nearby, we show inflation and real stock returns (stock returns adjusted for inflation) over 10 year horizons, for the period 1871 to 2021. We exclude periods of negative inflation or deflation (in the 1920s, the great depression, or the financial crisis of 2008), because the risk of deflation is quite different from the risk of inflation.

Inflation and Stock Returns (1871-2021)

Source: Shiller’s data; Stock returns represented by the S&P 500 index; 10 year rolling percentage returns and inflation rates, annualized.

As you can see from the left side, the correlation is generally negative, but not very strong, as there are periods of low inflation and low returns, and some periods with higher inflation and higher returns. (Inflation less than 3% is considered low. The Federal Reserve’s current target is an average inflation of 2%). On the right plot, we identify the observations that fall in the 1940s, 1970s, and 1980s in red. These are the three decades where inflation reached rates that were above average. As the chart illustrates, the relationship between stock returns and inflation tends to be stronger at higher levels of inflation, that is, when inflation becomes an important risk to manage.

How Important is Unexpected Inflation?

Simple correlations don’t tell us how important the effect of inflation is for a portfolio of stocks. For that, we need to quantify the impact of unexpected inflation on average real returns using past data. We find that an inflation surprise like the one we have experienced over the past year can lower average stock returns by one percent per year, over a five year period, after controlling for other macroeconomic factors like industrial production and the money supply.

Why is this Important and What Can You do?

Most financial plans are based on assumptions about expected returns from portfolios. Given that higher inflation can lead to lower real portfolio returns, it is important to consider the effect of lower returns on financial plans. A lower expected return means you have to save more, or for a longer time, to reach the same goal. We recommend increasing your savings accordingly. For example, if you are currently saving 10% of your income for retirement, increase that to 11% to offset the lower expected returns. We have suggested some tips and tricks to help you save more in a previous article. If saving more is not achievable, increase your retirement age by one year or reduce your future consumption. These actions can help you ensure that you stay on track with your plan. And if inflation subsides or real returns are not affected by inflation, you can make extra progress.

Considering the potentially negative effects of inflation on portfolio returns is particularly important for retirees in the first 10 years of retirement. The first five to ten years in retirement have an oversized influence on the likelihood of a successful spending strategy from the portfolio over a 30 year plan. While history shows that a spending rate of 4% of initial balance adjusted annually for inflation can work over periods of higher than average inflation, by slightly adjusting your spending in accordance with portfolio performance over the next five-ten years can help achieve higher spending rates over longer periods of time, like 25 or more years of retirement.

Portfolio Adjustments

For long term investors, the best protection against inflation is a broadly diversified portfolio. A lot of DIY investors end up building portfolios that are concentrated in the US market and particular industries within the US market. Market and global diversification can help reduce the correlation between US inflation and real stock returns. On the fixed income side of the portfolio, you can reduce the effects of inflation by investing in inflation-protected bond funds. These can include Treasury Inflation Protected Securities (particularly for retirement goals) and other bond funds with diversified exposure to corporate or municipal bonds, with an inflation protection overlay.

Inflation may or may not be transitory. By recognizing the potential risk in your plan you will be prepared in case inflation causes real portfolio returns to be lower than expected. And with a positive boost to your plan if it does not!

Massi De Santis is an Austin, TX fee-only financial planner and founder of DESMO Wealth Advisors, LLC. DESMO Wealth Advisors, LLC provides objective financial planning and investment management to help clients organize, grow, and protect their resources throughout their lives. As a fee-only, fiduciary, and independent financial advisor, Massi De Santis is never paid a commission of any kind, and has a legal obligation to provide unbiased and trustworthy financial advice. Massi is also a lecturer of finance and economics at Texas State University.