Why You Should Care About Your Retirement Income Strategy, and How To Find Opportunities to Generate More Income

Last week we talked about the economics of choosing between-taxable, tax-deferred, and tax-exempt accounts when funding retirement income. This week we want to give you a sense of how important making the right choices can be, and show you a prototypical example that helps illustrate how to find the right opportunities for efficient withdrawals.

Big differences in outcomes

To evaluate the many different strategies that you could use to withdraw from your taxable (T), tax-deferred (TD), and tax-exempt (TE) accounts, researchers start with assumptions about the values in different accounts, age, desired income level, social security, asset allocation, and market returns. They then try different combinations of withdrawals, taking into account income tax brackets and the different taxability of the different accounts (more on the economics here). The efficiency of each strategy is assessed by measuring the ending balance across accounts or the longevity of the portfolios — how many years of desired expenses was the strategy able to provide?

These experiments show that under a range of assumptions, differences across strategies are large. For example, in an experiment published in the Journal of Financial Planning, researchers tried 15 different strategies over 30 years for a 66-year-old couple with $2 million available to them, spread across T, TD, and TE accounts. The strategies differed in the order of the withdrawal from the different accounts, and some allowed for Roth conversions of differing amounts. Comparing the total balance at the end of the 30-year mark, the authors ranked the 15 strategies from best (1st) to worst (15th). They show that while some strategies ran out of money, optimal strategies ended with over $1.6 million in total account balance. The common rule-of-thumb of withdrawing sequentially from T, TD, TE was ranked 6th across the 15 and had less than $1.2 million in terminal balance.

What about longevity?

Measuring outcomes by the longevity of the savings shows similar results. Research shows that an optimal strategy can make your nest egg last up to six more years, from 30 to 36. This big difference can be very useful given current longevity trends. Under the rule-of-thumb strategy, the savings lasted 33 years. Better than other strategies, but not the best one.

It’s not about minimizing taxes

The research also shows that attempting to minimize taxes year-over-year should not be your goal. The strategies that generate the most income or last longer aren’t the ones that generate the lowest taxes. The best strategies can generate both more wealth and higher taxes over time. The goal of these strategies is to generate the highest level of sustainable income while minimizing tax drag in taxable accounts and the government share of the TD accounts. This is different from minimizing taxes per se. This result also highlights a key value that is added by a financial planner, who helps you get the most out of your resources over your entire life-plan, relative to a tax preparer, who may help you get the highest refund this year.

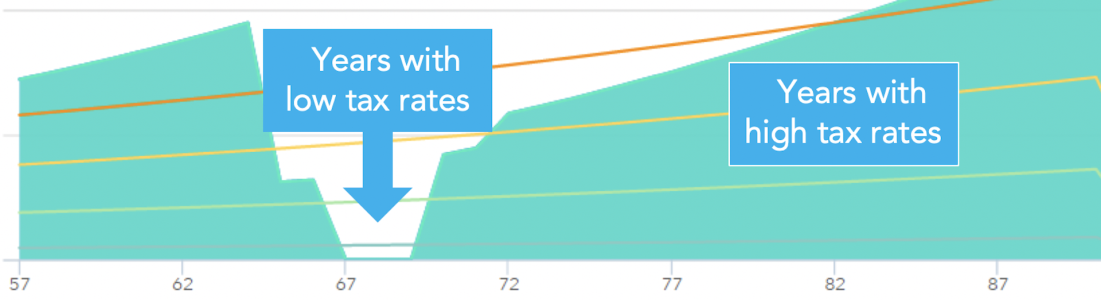

Visualizing opportunities

While a truly optimal strategy depends on individual goals and circumstances, economic principles and the cited experiments show that it generally includes some early TD withdrawals and Roth conversions to smooth out the marginal tax rate. Below, we show the example of a couple of retirees, both 66 years old, planning to start receiving social security when they turn 70. They have $1 million between their 401(k) accounts and $700K in their joint taxable account. Their desired expenses are $106K per year and have decided to postpone social security to age 70 when they will receive a combined benefit of $65,000. Their taxable income over time will vary with the chosen strategy. As a starting point, consider the taxable income under the rule-of-thumb strategy, shown by the green area in this figure, using the Right Capital software:

The picture shows how the couple can improve on this strategy. Notice that, initially, their tax rate is zero, as the income and capital gains generated from the taxable account are lower than the standard deduction, and there is no social security income. Instead of using the standard deduction ($27,400) on capital gains income, it would be more efficiently employed against ordinary income, withdrawing at least that amount from the 401(k) account. In addition, the figure shows that taxable income crosses the 22% (25% after sunset of the 2017 TCJA) when the couple reaches 72, due to required minimum distributions (“RMDs”) from the 401(k) accounts. Therefore, the picture is telling us that by filling up the 12% tax bracket in the first stage of retirement, the couple could reduce or eliminate the amount taxed later at 22%. This can be accomplished by making TD withdrawals and Roth conversions of the same amount until age 71, using funds from the taxable account to pay for the tax liability, as explained in a previous post. Doing so could reduce the marginal tax rate over the entire plan. And with the Roth conversion, the majority of any leftover amount would be tax-exempt at the end of the plan!

Your situation may be different, but given the potential gains from a strategy designed to your situation, it makes sense to plan ahead. Having the right strategy can mean less worry about running out of your savings because you lived longer than expected, a higher desired income for the ideal retirement you have planned, or a larger bequest to your loved ones or your favorite charity.

Until Next Time!

Massi De Santis is an Austin, TX fee-only financial planner. DESMO Wealth Advisors, LLC provides objective financial planning and investment management to help clients organize, grow, and protect their resources throughout their lives. As a fee-only, fiduciary, and independent financial advisor, Massi De Santis is never paid a commission of any kind, and has a legal obligation to provide unbiased and trustworthy financial advice.

{kind=link}