A key goal when you retire is to generate a steady level of spending and not run out of money too soon. For many, the retirement spending strategy involves a combination of social security, taxable accounts (T), tax-deferred accounts (TD) like 401(k)s or IRAs, and tax-exempt accounts (TE) like Roth accounts. Because of the different taxability across accounts, how you withdraw from them can make an important difference to the level and longevity of your retirement spending. Research shows large differences in ending account balances or the expected number of sustainable years across different strategies.

A common rule of thumb is to first exhaust the taxable accounts, then tap into the tax-deferred, and finally the tax-exempt accounts. However, blind application of the rule can be costly. A better approach is to start with some key economic principles driving the decision, then apply them to your particular situation.

Economics

Two key principles can help guide our decisions. First, there is a tax-drag to growth in taxable accounts, and not in TD or TE accounts. Second, it helps to think of your TD accounts as a partnership with the government, where the government portion equals the marginal tax rate at the time of withdrawal. Remove that portion, and the remaining part, your portion, grows tax-exempt, just like a TE account.

The first principle says that your dollar in TD or TE accounts will grow faster than your dollar in a taxable account. The second principle gives you an incentive to find opportunities to lower the portion of the TD account that belongs to the government.

The common withdrawal sequence T, TD, TE, is not a good application of the second principle. It ignores that there are opportunities to turn some TD savings into tax-free or low-tax income, and the fact that larger withdrawals later on from TD accounts (including RMDs) can put you in higher income tax brackets.

Application

Here are a few steps that you can take to apply the basic economic principles to your case. However, keep in mind that you should consult with a tax professional before putting them into practice, as your particular situation may require additional considerations.

Set goals

As usual, a good strategy should start with your goals. Your desired expenses and tax situation should give you an indication of the range of tax brackets you will face. If you plan to leave excess funds to a beneficiary, consider their tax rate. For example, the second principle implies that if you expect your tax rate (or the beneficiary’s) to be lower by the end of the plan you have an incentive to use TE assets before TD assets. If you expect the rate to be higher later in retirement, you have an incentive to use TD assets before TE assets.

Identify Opportunities for Tax-efficiency

Once we understand the incentives (reduce tax drag to growth, increase your portion of TD) and our goals, the next step is to find opportunities to get the most out of your savings.

Consider income tax deductions, for example. For a married couple filing jointly with both spouses over the age of 65, the standard deduction is $27,400 for 2020. This is an opportunity to withdraw the first $27,400 from the TD account tax-free. The next $19,750 is taxed at 10%, and the next $60,500 is taxed at 15%.

If this hypothetical couple used the rule of thumb of exhausting the taxable account first, they would give up part or all of the benefit of the standard deduction available to them, as taxable income from the taxable account could be minimal or zero.

Smooth your tax bracket

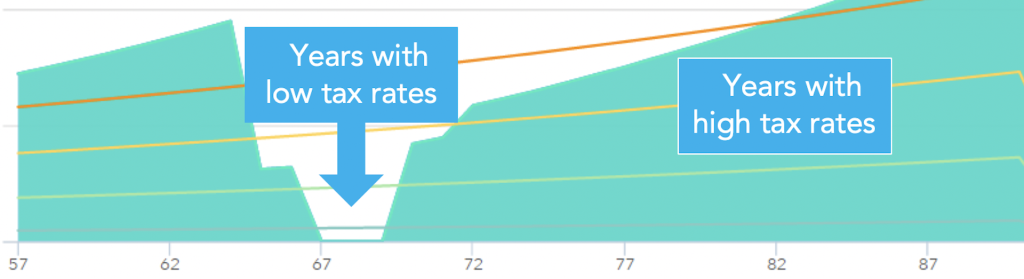

Withdrawing from TD early helps you keep your income tax rate smoother and lower. A couple that expects to be in the 24% bracket if all income came from a TD account can benefit from withdrawing at the 10% or 15% tax rate early on. This will help you lower the taxable portion of your TD. It’s likely that early in your retirement, particularly if you delay social security, that your taxable income without a TD distribution is unusually low. Use this period to make tax-free and low-tax TD withdrawals.

Convert the TD withdrawal to Roth

In addition, you can convert your entire TD withdrawal to Roth. Say you make a $10,000, 15% marginal-tax withdrawal from your TD account. You can deposit the $10,000 to a Roth account by paying a $1,500 tax liability from your taxable account. Why do this instead of using part of the TD withdrawal to pay for the tax? Because the $1,500 will grow tax-free in a Roth, while it is taxed in a taxable account. The TD withdrawal gives you the opportunity to lower your tax bracket over time and to reduce the tax drag from your taxable account. This is why, even if your tax rate is constant over time, Roth conversions may make sense.

TD vs. TE

Conventional wisdom is to use TE first if you expect your tax bracket to go down and use TD first if you expect your tax bracket to go up. There is some truth to that. However, as we saw above, our withdrawal strategy can have a big impact on our tax-bracket. If the goal is to make the savings last longer, it can help to make TD withdrawals to fill up the tax-free and low tax brackets (how much depends on your situation), then use TE to stay in the lower tax bracket for as long as possible. Remember that both accounts are equally efficient in terms of growth. Therefore, by smoothing and reducing the average tax bracket over time, your savings can last longer. Research from Baylor University and Texas Tech confirms the benefits of this strategy with simulated examples.

The above may not always be best if there is a bequest motive, in which case it is important to consider the tax bracket of the beneficiary. But the economic principles still apply. It may also be desirable to have some TD assets for potential situations where you may be in an unusually low tax bracket. One example can be towards the end of a financial planning horizon where you may need to fund large, long-term care expenses. TD assets could be used efficiently for this purpose.

It’s impossible to cover every situation to figure out what the optimal strategy is for each individual in a short article. Therefore, you should not view this discussion as tax advice and consult a tax professional to determine the best course of action for you. However, we think that an understanding of these key economic principles can help you make a more informed decision and avoid blind application of simple rules of thumbs. As always, shoot us an email or schedule a call if you would like to explore this or other planning questions more thoroughly.

Until Next Time!

Massi De Santis is an Austin, TX fee-only financial planner. DESMO Wealth Advisors, LLC provides objective financial planning and investment management to help clients organize, grow, and protect their resources throughout their lives. As a fee-only, fiduciary, and independent financial advisor, Massi De Santis is never paid a commission of any kind, and has a legal obligation to provide unbiased and trustworthy financial advice.