Understand The Social Security Tax Torpedo And What You Can Do About It

Photo by U.S. D.O.D. graphic by Ron Stern. (RELEASED) / Public domain

Don’t worry, we are not talking about the chances of a blow-up of the Social Security fund. We are talking about the interaction between the taxation of Social Security and other sources of income, and potentially high tax rates resulting from it.

If you have ever looked at your Social Security statement, it shows your expected benefit at retirement. But have you thought about if and how it will be taxed? Benefits were not taxable prior to 1983, when that changed and Congress created a system that’s relatively complicated and nonlinear. If you hit certain income thresholds, which we review below, your marginal tax rate can jump, even above the 37% rate, and for relatively low-income levels, an effect called the Social Security “Torpedo.” Avoiding the torpedo should be part of an efficient retirement withdrawal strategy. To do that, let’s review some basics of Social Security taxation.

Social Security Taxation

Whether your Social Security benefit will be taxed in a given year depends on your “provisional income” for the year. That is the sum of your income from all sources plus half of your Social Security benefit, subject to other adjustments.

Provisional Income = ½ Social Security Benefit + Other Income

| Taxability of Benefit | Married Filing Jointly | Single Filer |

| Exempt | PI Less than $32,000 | PI Less than $25,000 |

| Up to 50% | PI b/w $32,000 and $44,000 | PI b/w $25,000 and $34,000 |

| Up to 85% | PI Greater than $44,000 | PI Greater than $34,000 |

For married couples filing separately, 85% of the benefit is taxable. Notably, these thresholds have not been adjusted for inflation since 1993, meaning every year a greater fraction of benefits across the population get taxed. How much of the benefit is taxable is computed using a step-function that has limits of 50% or 85% of the benefit depending on where provisional income falls.

Example

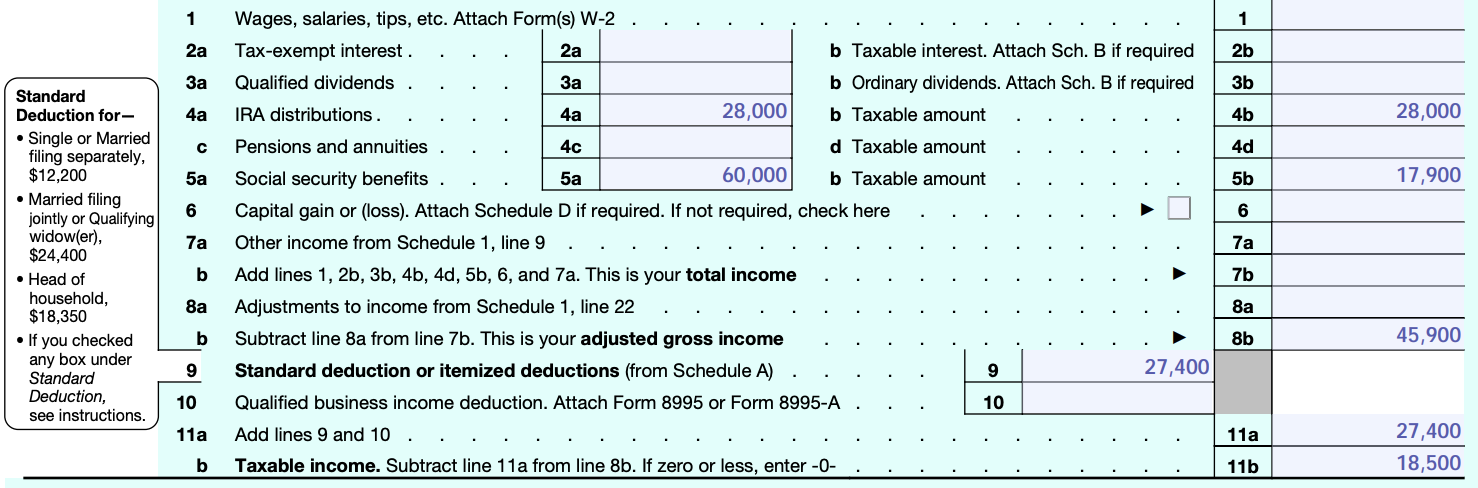

Consider a married couple with combined benefits of $60,000 and $18,000 traditional IRA income. Provisional income is $48,000 = $30,000 + 18,000. In this scenario, using IRS formulas, the amount taxable is $9,400. Thus, the adjusted gross income is $27,400. The standard deduction for the couple is also $27,400 for 2020, so the couple owes no income taxes.

The Torpedo

Suppose the couple withdraws an additional $10,000 from their IRA to supplement expenses, for a total of $28,000. Their provisional income is now $58,000 and their taxable benefit amount goes up by $8,500 to $17,900. Notice that while their pre-tax income increased by the $10,000 withdrawal, taxable income increased by $18,500! While their marginal tax rate bracket is 10%, the effective marginal tax rate on the $10,000 is 18.5%. This happens because every $1 of additional pre-tax income increases taxable income by $1.85, as more of the Social Security benefit gets taxed. The table below summarizes this example.

| Ex: Married Filing Jointly | Case 1 | Case 2 |

| Soc. Sec. Benefit | 60,000 | 60,000 |

| IRA Income | 18,000 | 28,000 |

| Taxable Benefit | 9,400 | 17,900 |

| Adjusted Gross Income | 27,400 | 45,900 |

| Deduction | 27,400 | 27,400 |

| Taxable Income | 0 | 18,500 |

| Tax | 1,850 | |

| Marginal Tax Bracket | 10% | |

| Effective Marginal Rate | 18.5% |

And this is what Case 2 looks like in a 2019 1040 form.

What To Do About It, Meet With a Fee-Only Fiduciary in Austin Texas, Desmo Wealth

I chose a simple example above to illustrate the fact that an additional $1 of pre-tax income brings about a greater increase in taxable income. However, things can get worse than the example above for income higher tax brackets. Notice that the 18.5% tax rate can be completely avoided if the withdrawal was instead from a Roth IRA account. Roth IRA withdrawals do not count as part of provisional income and do not affect the taxability of Social Security benefits.

The same is true for HSA withdrawals if used for health-related expenses. In general, the taxability of Social Security benefits should be considered within an efficient retirement income strategy. The Social Security Tax Torpedo highlights the importance of building up different buckets to help you smooth your tax rate in retirement.

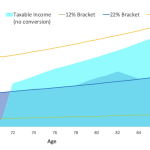

The first step is laying out what taxable income will look like over time, based on needs and sources of income, then use this projection to find opportunities to smooth out your marginal tax rate. For example, in years where you may have deductible expenses, like healthcare-related expenses, you can make larger withdrawals from tax-deferred accounts like the IRA or your 401(k). In addition, consider doing Roth conversions in years when your marginal tax rate is lower. That will help you lower your taxable income when you have to make the 401(k) or IRA withdrawals.

Everyone’s situation is different, and will likely depend on a host of other factors not considered here. But hopefully this piece of information will help you get started on your way to a more efficient retirement income strategy, avoiding torpedoes!

Until Next Time!

Massi De Santis is an Austin, TX fee-only financial planner. DESMO Wealth Advisors, LLC provides objective financial planning and investment management to help clients organize, grow, and protect their resources throughout their lives. As a fee-only, fiduciary, and independent financial advisor, Massi De Santis is never paid a commission of any kind, and has a legal obligation to provide unbiased and trustworthy financial advice.

{kind=link}