The CARES Act is an economic relief plan for individuals and businesses of unprecedented size, totaling about $2 trillion. As a comparison, the 2019 US GDP was about 21 Trillion. The Act is very broad and includes many different programs aimed at reaching broad sections of the economy. Our goal is simply to inform readers and clients of parts of the Act that may affect their financial plans, not to dig deep. This commentary should not be viewed as tax advice. Consult with your advisor or tax professional, or schedule a call with us if you think any of the items we discuss may impact you, or want to learn more.

Taxpayers’ Recovery Rebates

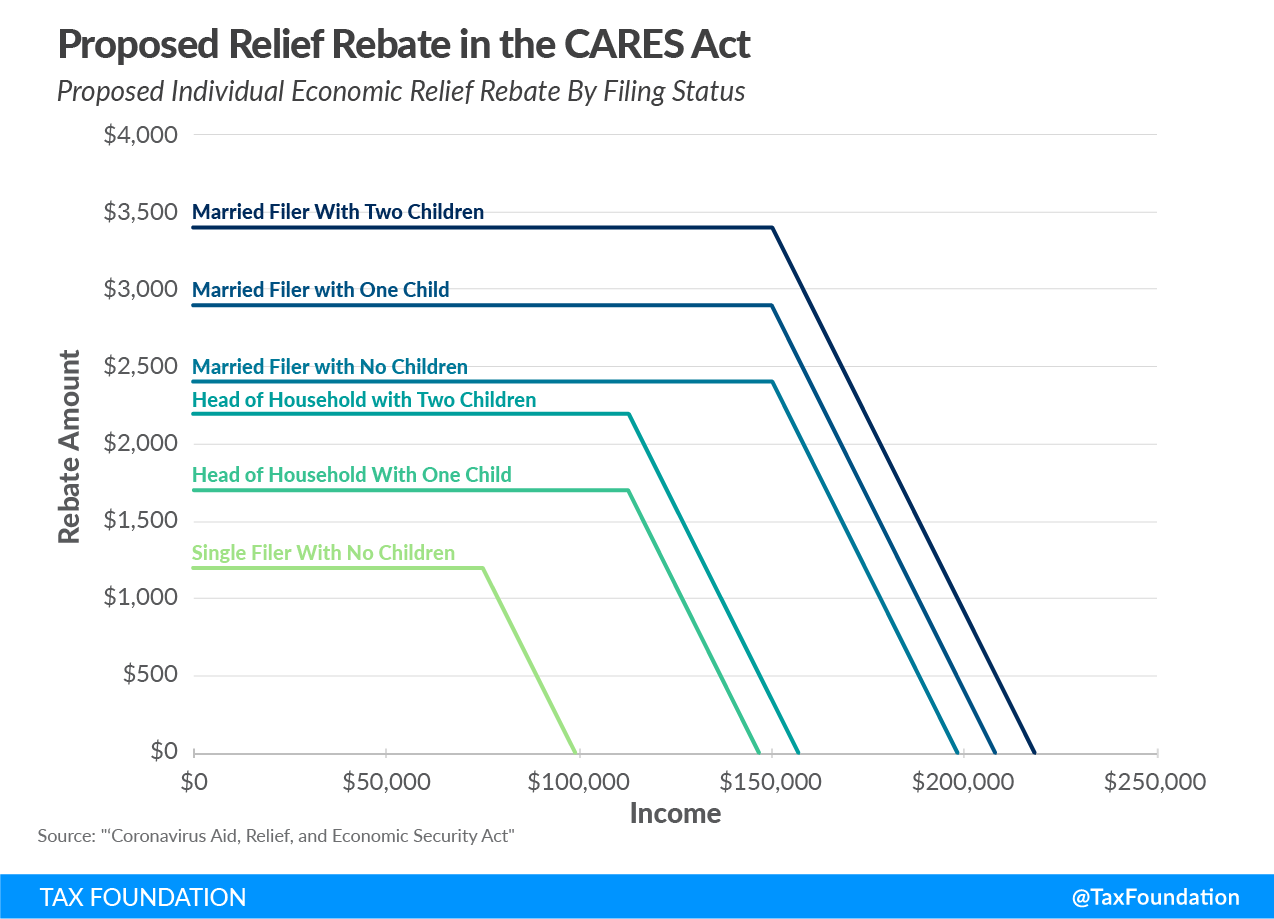

This is the item that has garnered the most attention. Taxpayers may receive tax rebates up to $1,200 for single filers and up to $2,400 for married filing jointly. The credit amount is further increased by up to $500 for each child under the age of 17. The rebates are phased out according to the following schedule.

The Tax Foundation estimates that over 90% of filers will get a rebate, and nearly all filers below the 80th percentile of income.

If you have not filed for 2019, consider filing now if your 2019 income is lower than 2018. Otherwise you can decide to wait until July 15. The tax rebate will be based on the latest income tax return that you filed (2018 or 2019). A lower income may give you a higher rebate. The final rebate amount will depend on 2020 income (with tax returns filed in 2021). Taxpayers who receive a smaller rebate than they are eligible for based on 2020 income will receive the difference after filing a 2020 tax return, but overpayments of rebates due to a higher income in 2020 will not be clawed back.

Distributions and loans from retirement plans

The act relaxes requirements for qualified distributions under employer sponsored plans and IRA accounts. Up to $100,000 can be withdrawn in total across such plans by someone affected by the Coronavirus. The withdrawals will be:

- Exempt from the 10% penalty for early withdrawals;

- Exempt from normal withholding requirements;

- Eligible to be repaid over 3 years;

- And the resulting income distribution can be spread over three years.

The act also relaxes some of the constraints on loans from retirement plans. Loan amounts are increased to $100K and 100% of the vested amount can be withdrawn.

Relief for Student Loan Borrowers

Student loan payments on federal student loans are deferred until Sept 30, 2020. Over the six months, no interest is accrued on the loans. You have to proactively suspend the payments. So, if you have a federal student loan, call your provider to suspend them. If you think you may qualify for student loan forgiveness, you may want to suspend the payments in case the loan is forgiven in the future.

The act also contains a special provision that allows payments of student loans by employers to be excluded by taxable income, up to the $5,250 amount typically allocated to employer educational assistance programs. If your employer has an educational assistance program, ask them if they are willing to include student loan repayments for you this year.

Small Business Help

The act contains a number of programs to help small businesses affected by the coronavirus. Here is a rundown. Check the SBA website for details and to apply. The criteria are intentionally broad, so if you are a small business affected by COVID-19, chances are there is a program for you. One catch is to apply early, as some of these may be on a first-come first-served basis. Check out our instructional video to apply for a disaster relief loan on the SBA website.

Paycheck Protection Program

Small businesses may take out loans to help pay for payroll costs, health insurance premiums, rent, mortgage interest, and other costs. A portion or all of the loan may be forgiven if used in the first eight weeks on eligible expenses. In addition, the maximum interest rate that can be charged for a loan made under this program is 4% and the term of the loans can be up to 10 years. That can be a good rate for many small businesses. Finally, payments on these loans can be deferred for six months.

The SBA has additional programs to help small businesses, so we encourage you to check them out.

Employee Retention Credit and deferral of payroll tax payments

Employers whose activity was partially or completely suspended may be eligible for a payroll tax credit. The credit is equal to 50% of wages paid to each employee, up to a maximum of $10,000 of wages per employee, subject to caveats.

In addition, according to the Act, employers are able to defer payroll taxes through the end of 2020, until the end of 2021 and 2022. Specifically, 50% of the payroll taxes that would otherwise be due throughout 2020 can be deferred until December 31, 2021. The remaining 50% is due on December 31, 2022.

Net Operating Losses (NOL) rules

The CARES Act allows NOL from 2018, 2019, or 2020 to be carried back up to five years. This should allow companies to reduce prior years’ tax bills, allowing them to claim refunds of amounts previously paid to provide further liquidity to get them through the COVID-19 crisis. The law allows for up to 100% of taxable income to be offset for 2018, 2019, and 2020.

Waived Required Minimum Distributions (RMDs) from retirement accounts

The Act eliminates any RMD that needs to be taken in 2020. If you have taken your RMD within 60 days, you can roll it over to your retirement account by the end of the 60 days window.

Increased tax deductions for charitable contributions

Charitable contributions may drop during this crisis period. To reduce this drop, the Act introduces a new above-the-line deduction (directly reduces your adjusted gross income or AGI) of $300 for charitable contributions. In addition, the AGI limit for cash contributions (currently limited at 60% of a taxfiler’s AGI) is raised to 100%.

Increased unemployment benefits

The Act gives a substantial boost to unemployment benefits. The first week of unemployment is now covered. In addition, there is a boost to the benefits of $600 a week, and a 13 week extension beyond the normal duration determined at the state level (26 weeks in Texas).

Overall, the CARES Act addresses a number of key issues that individuals and businesses are facing right now as a result of COVID-19, so it is a welcome development. Take a look at the list and the links provided, and consult your tax professional or financial advisor to learn more. Act quickly, as some of these programs have time limits or are on a first-come-first-serve basis.

Until Next Time!

Massi De Santis is an Austin, TX fee-only financial planner. DESMO Wealth Advisors, LLC provides objective financial planning and investment management to help clients organize, grow and protect their resources throughout their lives. As a fee-only, fiduciary, and independent financial advisor, Massi De Santis is never paid a commission of any kind, and has a legal obligation to provide unbiased and trustworthy financial advice.